Speak with an experienced advisor!

Speak with an experienced advisor! So you want to retire early?

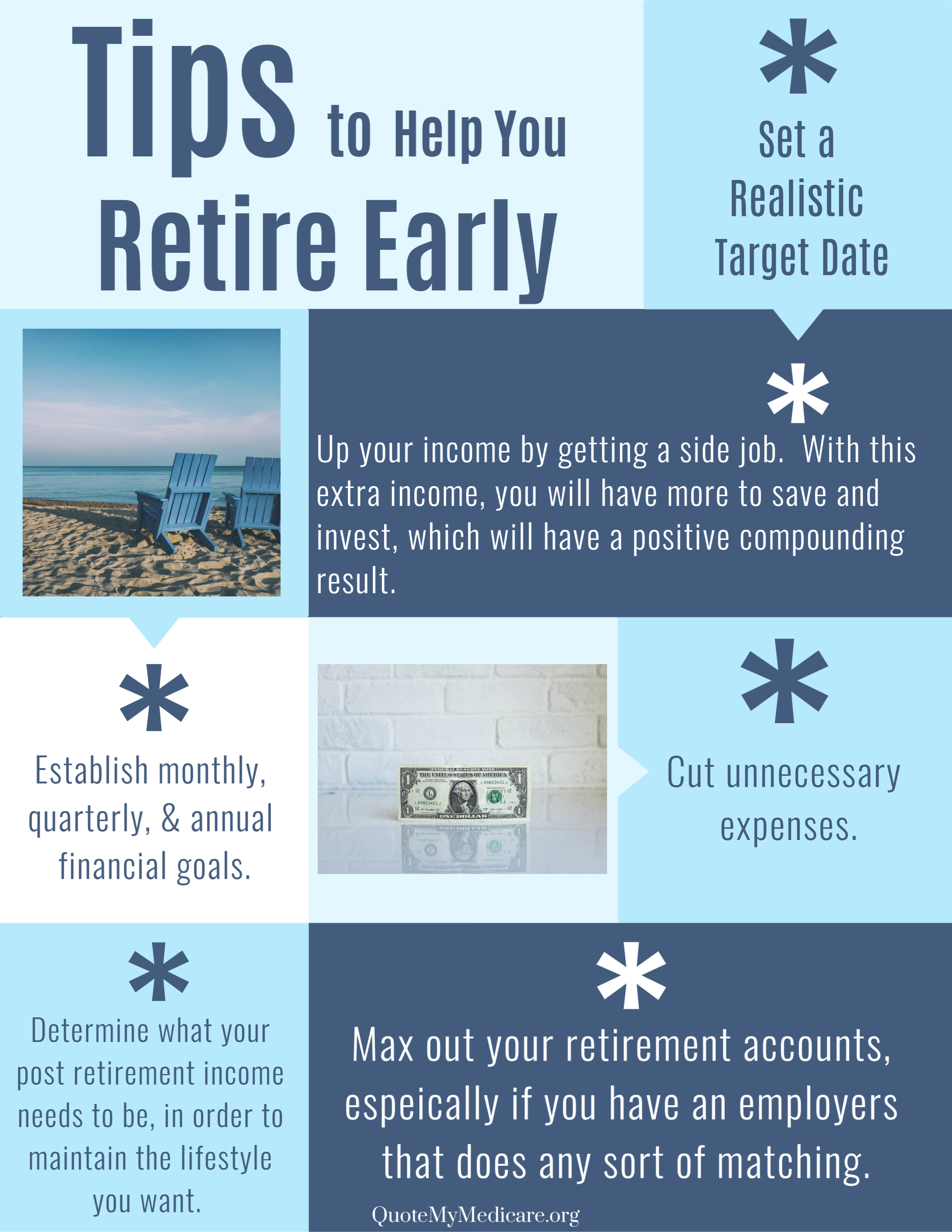

More people these days are working to an older age than ever before. In order to retire early, you must have a pretty good plan.

Even with so many continuing to work in their late 60’s and 70’s, being able to retire early might not be as hard as you think. Like most things in life, early retirement requires having a plan. Below are several tips that can help you reach this coveted milestone.

Should You Make Extra Mortgage Payments

Ultimately, when you cut unnecessary cost, using the extra money in order to pay down debt is always a good strategy. Dave Ramsey talks about using the debt snowball method, which is an excellent strategy. In essence, you start paying off smaller debts first, and as you payoff one debt, you roll that payment into the next debt. Using this method, once you knock out common debts like credit cards, and auto loans, then you can snowball all of those monthly payments into paying off your mortgage much earlier than just making the minimum mortgage payments. The best way to get this all started, is by cutting unnecessary cost, and adding that extra money into your monthly payment of your smallest debt.

Impact on Social Security

One important thing to remember is that if you take Social Security early, you will have a much lower payout. If you were born after 1960, the full retirement age has increased to 67. Keep in mind, you can still start taking Social Security Retirement Benefits at age 62, but benefits will be significantly lower.

Health Insurance Cost

One last important factor to consider is healthcare cost. Most people do not qualify for Medicare until age 65, so if you retire early, you will most likely need health insurance off the individual healthcare market. This coverage is typcially not that great, and is also pretty expensive. Make sure you crunch the numbers, so rising healthcare premiums don’t force you to have to do the unthinkable……….go back to work!